Interest evokes strong reactions across the globe, from developed to developing nations, affecting people in vastly different ways—those on Wall Street versus Main Street, capital owners versus borrowers, and heirs of wealth versus wage earners. Given its central role as both a financial lever and a policy tool for central banks, it is worth reexamining whether interest must remain as essential and inevitable as we have long been taught to believe.

This series of articles explores how interest shapes lives and economies worldwide and imagines what the world might look like if interest no longer existed—if it ceased to be a defining element in financial theories, economic models, and the decisions made by individuals, businesses, societies, and nations.

When The Price of Time Breaks

The modern economy revolves around a deceptively simple idea: interest is the price of time. It decides whether investment happens, housing remains affordable, governments can spend, currencies stay stable, and crises spread across borders. Few economic concepts reach so deeply into everyday life while remaining so abstract.

Imagining a world without interest is not idle speculation. It exposes how much of modern economic behavior depends on a single mechanism for coordinating the future. Interest is designed to balance patience with risk, saving with investment, and present sacrifice with future reward. When the system works, interest is almost invisible; when it fails, it overshadows everything.

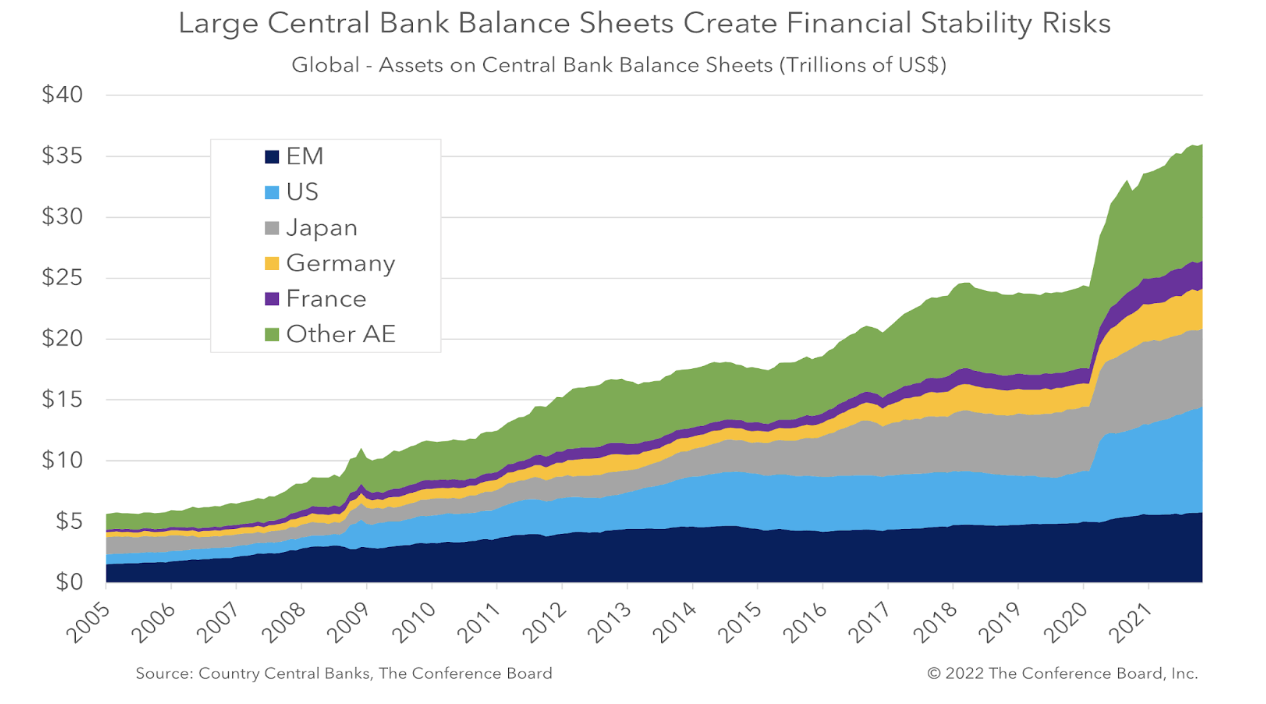

Recent history offers a revealing experiment. For much of the decade after the global financial crisis, interest rates in major economies hovered near or below zero. That era was followed by one of the sharpest and widest tightening cycles in modern times. These two extremes expose an uncomfortable truth. When interest nearly disappears, the economy becomes more financialized, more dependent on asset prices and fragile confidence—rather than more equitable or productive. When interest surges back, it does not simply restore equilibrium; it suppresses real activity, amplifies inequality, and spreads stress worldwide.

Interest, then, is not merely a technical policy instrument. It is an organizing principle that dictates who bears risk, who earns returns, and how societies adapt to shocks. Yet this reliance creates tension: an economy that depends too heavily on interest to coordinate time may become unstable—whether rates are too low or too high.

The Near-Zero Interest Decade - What Can We Learn?

Between the global financial crisis and the mid-2010s, the price of short-term money in major economies remained pressed against its lower bound. In the United States, the Federal Reserve held the federal funds rate near zero—between 0.00 and 0.25 percent—from December 2008 until the first rate increase in December 2015.

In the euro area, the European Central Bank went even further, pushing key policy rates into negative territory. Holding idle cash no longer earned a return; instead, it was subtly penalized to encourage households, banks, and firms to put money back to work. The ECB’s deposit facility rate first dipped below zero in June 2014 and gradually declined to minus 0.5 percent by September 2019. Japan took the experiment to its limit. The Bank of Japan introduced a negative policy rate in 2016 and maintained ultra-low rates for years before finally exiting negative territory in March 2024, raising its policy rate to between 0 and 0.1 percent.

These episodes provide a powerful real-world test of what happens when interest rates lose much of their role in guiding financial behavior. Credit, borrowing, and investment continued, but the price of capital ceased to be the key signal directing activity. With the cost of money near zero, one crucial friction disappeared—allowing other forces to dominate, particularly asset prices, expectations, and balance-sheet dynamics.

The period also revealed an important truth: a world of exceptionally low interest rates is far from calm or neutral. In such an environment, small shifts in confidence or prices have outsized effects because borrowing is easy, leverage builds quickly, and financial values weigh more heavily on economic choices. In practice, asset owners gain first—through rising housing and stock prices—while those without assets see little improvement in daily costs or opportunities, leaving many with the uneasy sense that cheap money circulates freely but works for someone else.

How Does Low Interest Rates Change Everyday Life?

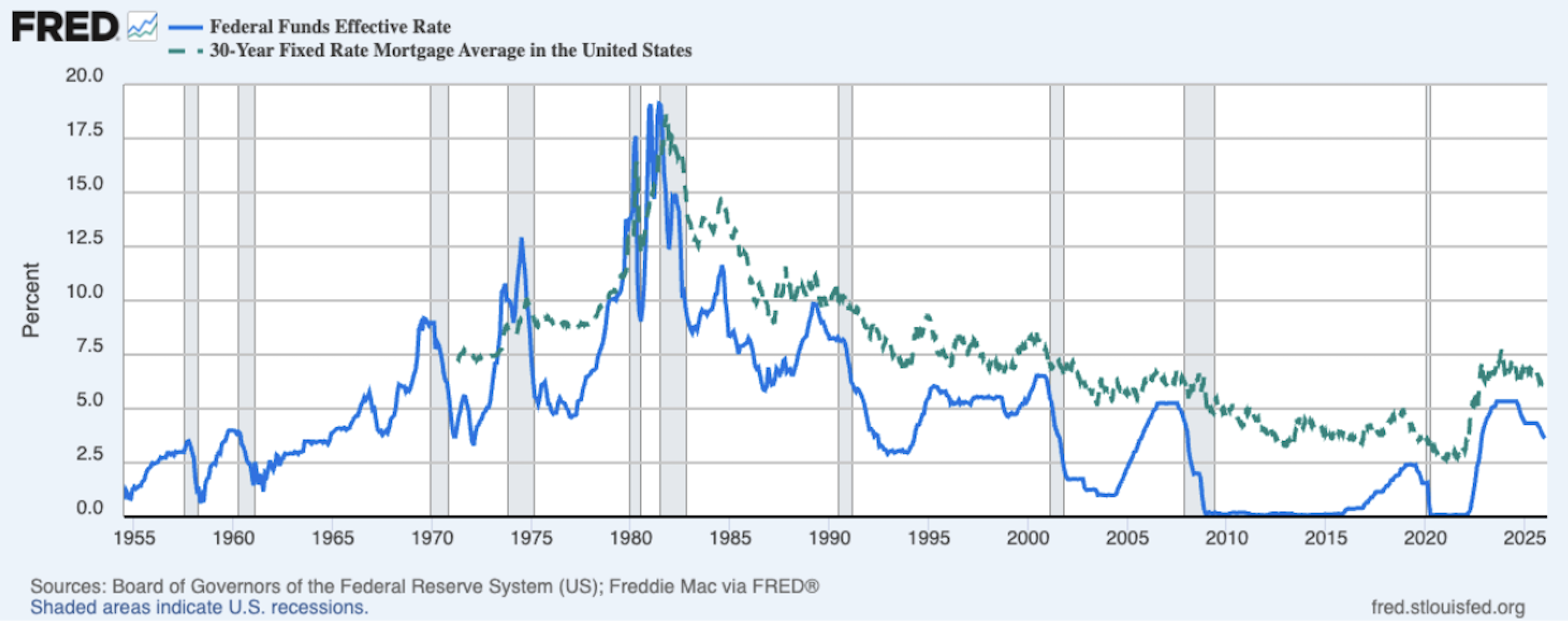

Source: FRED, how Mortgage responds to interest rates

Low interest rates are a real-economic force that shapes everyday behavior. When borrowing costs fall, loans become cheaper and monthly payments lower. For most households, i.e.much of the population, this can make a big difference: mortgages, student loans, and small business financing become more manageable, while major life decisions like buying a home, starting a business, or moving for work feel more attainable. Lower rates also ease budget pressures, freeing up money for spending, saving, or improving living conditions, opportunities that are often.

out of reach in periods of high interest. As a result, low-rate environments are commonly associated with stronger employment, fewer defaults, and better financial health for households that rely more on wages than on wealth.

In such economies, prices for goods and services usually rise slowly, making the cost of living more predictable even if incomes grow modestly. Predictability—rather than rapid improvement—becomes the defining feature. Over time, this stability changes people’s expectations. With borrowing costs being low, households and small businesses can think beyond day-to-day survival and plan. In this way, low interest rates not only aid the economy but also reduce financial strain for those focused on affordability rather than profit.

This understanding helps explain why the return of high interest rates feels so punishing to many. What changes is not only the cost of money—but the small margin of security and breathing room that allowed ordinary people to plan, aspire, and move forward.

Speculation And the Uneven Impact of Interest Rate

Speculation is often misunderstood as something separate from the real economy, but in a low-interest world, it becomes more visible for a simple reason. When safe returns are small, people with large amounts of money worry less about earning a steady income and more about timing. They buy assets not just because borrowing is cheap, but because they believe low interest rates will not last forever, and prices may rise before conditions change. This kind of activity first shows up in financial markets, not because they are more important or more worthy, but because they can act faster. Households and small businesses cannot function as quickly because they need stable income, long-term planning, and the knowledge that they can follow through on their commitments. Big financial institutions can move money fast, assume risk, and turn around when expectations change.

For this reason, speculation itself should not be the focus of concern. What matters far more is what happens when interest rates are raised in response to financial or policy pressures. Speculative positions can usually be adjusted, reduced, or unwound quickly. Ordinary households cannot. The people who organized their lives around low interest rates did so through mortgages, education, small businesses, and everyday budgeting, not short-term trades. When interest rates are increased, the impact is not evenly distributed. Financial markets are affected first, but the effects are seen for a much longer period on households. The cost of borrowing rises, and it becomes difficult to get a job. Plans that seemed feasible in the past become uncertain. The problem is not that there was speculation, but that the effects of tightening reach people who were not speculating.

When interest plays a smaller role in shaping economic decisions, everyday activity naturally carries more weight. Households and small businesses operate on stability and long-term planning, not speed or constant repositioning. In such a setting, success depends less on timing financial moves and more on producing, working, and sustaining activity over time. This does not remove finance from the economy, but it reduces how much advantage comes from reacting quickly to policy changes, allowing real economic participation to matter more.

Why Low Interest Produced Different Outcomes Across Advanced Economies

The decade of low interest rates did not yield uniform results across advanced economies, because rates were only one part of a much wider policy and institutional landscape.

In the United States, near-zero rates coincided with large-scale asset purchases and, later, substantial fiscal support. The Federal Reserve explicitly described its post-2008 strategy to lower long-term borrowing costs, stimulate credit, and strengthen employment. Labor markets rebounded more quickly than in many peer economies, and asset prices rose sharply.

In the euro area, negative rates and asset purchases were also introduced, but their effects differed across member states. Structural divides—fragmented banking systems, unequal fiscal capacity, and institutional constraints—meant that cheap money did not translate as clearly into investment or job growth. The European Central Bank itself described its move into negative rates as gradual and cautious, reflecting concerns about bank health and financial stability.

Japan presents another variation. It maintained ultra-low and negative rates for far longer than others but still struggled to achieve sustained inflation or strong growth. When the Bank of Japan finally exited negative rates in March 2024, it closed a long-running experiment that underscored how persistent weak demographics and productivity can undermine monetary stimulus.

Taken together, these experiences highlight a key lesson: low interest rates are not a growth engine in themselves. They magnify the structural features already in place. Where institutions, fiscal policy, and productivity are strong, low rates can reinforce progress. Where they are weak, low rates mainly inflate asset values and deepen reliance on central banks.

The Definition Problem Exposes the Low-Rate Decade

A prolonged period of low interest rates also reveals the limits of conventional economic indicators. Gross Domestic Product (GDP) measures the value added in producing goods and services over time. It remains a vital metric, but it does not clearly distinguish between growth driven by productive investment and growth fueled by financial activity or rising asset values.

Inflation, typically captured through Consumer Price Index (CPI) measures, focuses on the prices of consumer goods and services. As a result, asset price surges can be enormous in economic impact yet remain largely invisible in headline inflation. This helps explain why the 2010s appeared stable in official data even as inequality and financial risks quietly expanded beneath the surface.

Unemployment presents similar limitations. Under the International Labor Organization’s definition, a person must be without work, available for work, and actively seeking work to count as unemployed. Even in robust labor markets, this means unemployment can never truly fall to zero. The low-rate decade made this clearer by drawing attention to underemployment, labor force participation, and job quality—factors that headline unemployment figures often obscure.

These definitional boundaries are not flaws. They simply matter more in an economy where the most significant movements occur through finance and balance sheets rather than through prices on store shelves.

From Cheap Money to Constraint: Why Today Feels Different

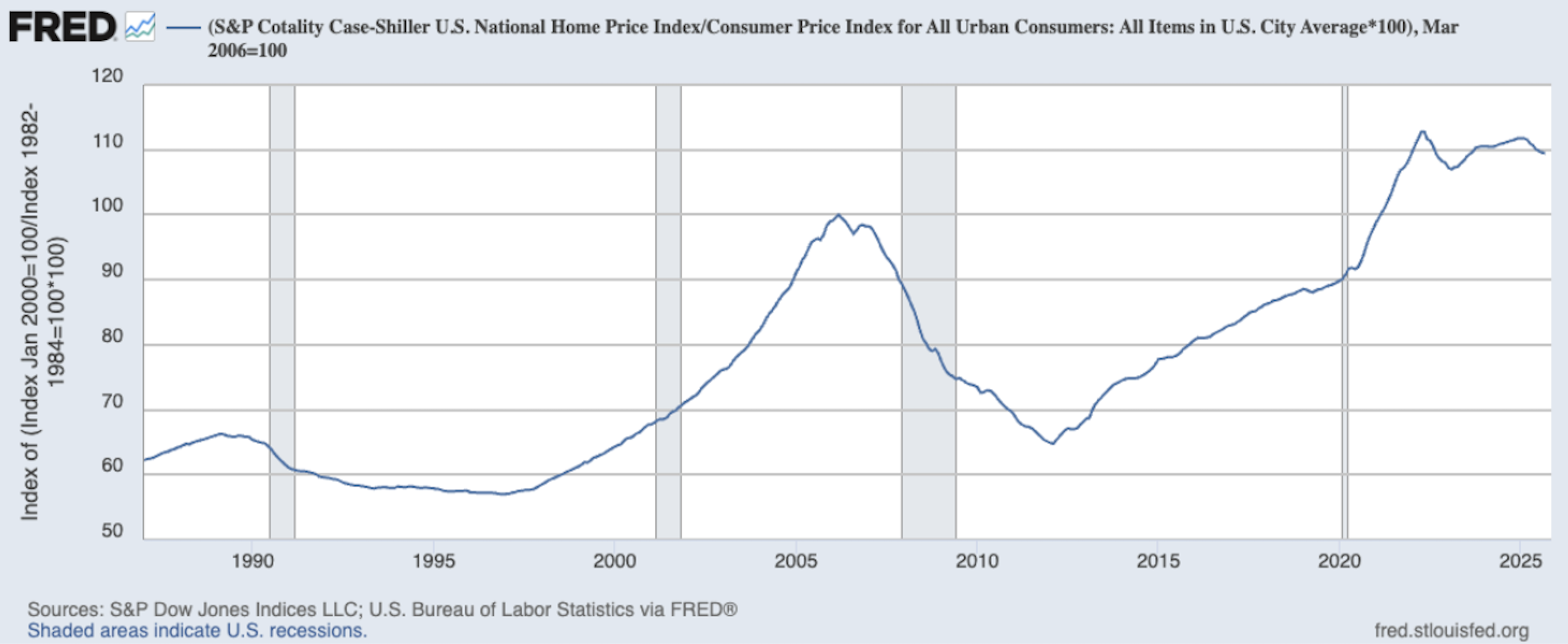

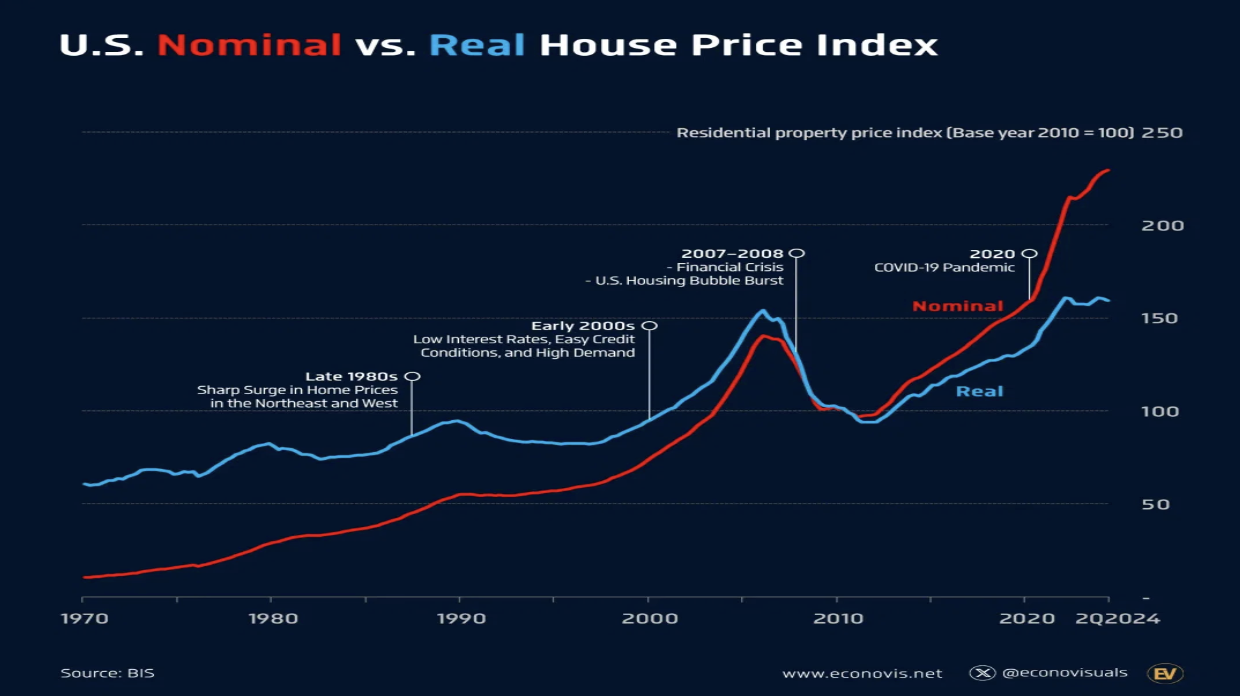

The move away from near-zero interest rates has exposed how heavily the real economy had come to rely on cheap money. Since 2022, policy rates in the United States have climbed above 5 percent—the fastest tightening cycle in decades. Mortgage rates followed suit, with the average 30-year fixed rate jumping from roughly 3 percent in 2021 to over 7 percent by 2023.

The result has been a steep decline in affordability and a marked slowdown in housing activity, even as nominal home prices have remained high. This combination is particularly damaging: transactions fall, construction slows, labor mobility weakens, and investment becomes harder to justify.

The current environment feels especially disheartening because high interest rates now coexist with sluggish productivity growth, aging populations, and heavy debt burdens. Unlike the early 1980s, when high rates were deployed to break persistent inflation and paved the way for years of expansion, today’s elevated rates seem less like a cure and more like a constraint. Real interest rates remain positive even as inflation recedes, keeping financial conditions tight and dampening the willingness to invest.

Why The 1970s Analogy Breaks Down: A Comparison That Only Goes So Far

The 1970s are often invoked when discussing high interest rates, but the comparison must be managed carefully. In the late 1970s and early 1980s, nominal interest rates were extremely high. The US federal funds rate peaked above 19 percent in 1981. Yet inflation was also extremely high, meaning real interest rates were not uniformly restrictive until the disinflation process took place. The Volcker tightening was painful, but it occurred in an economy with strong demographic growth and rising productivity potential. Once inflation expectations were broken, interest rates could fall, and a long expansion followed.

Today’s environment is different. Inflation rose rapidly after the pandemic, but largely due to supply disruptions and energy shocks rather than a classic wage-price spiral. High interest rates are now suppressing demand in an economy that lacks the growth engines of the post-war era. That difference explains why the same policy tool feels far more depressing now than it did in earlier high-rate episodes.

How Interest and The Dollar Transmit Stress to Developing Economies

The burden of high interest rates falls even more heavily on developing and emerging economies. Much of their external debt is denominated in U.S. dollars, so when U.S. interest rates rise and the dollar strengthens, the local-currency cost of servicing that debt increases sharply.

According to World Bank data, a large share of developing-country external debt is dollar-based. During periods of aggressive U.S. monetary tightening, capital tends to flow toward dollar assets, emerging-market currencies weaken, and central banks are often forced to raise their own rates defensively—even when domestic demand is already fragile.

This pattern is not new. In the early 1980s, U.S. tightening helped trigger the Latin American debt crisis by driving up debt-service costs and compressing growth. While today’s circumstances differ, the underlying dynamic remains similar: high interest rates at the core of the global financial system transmit stress outward through exchange rates and capital flows. For many developing economies, this means imported tightening, slower growth, and shrinking fiscal space—just when investment and social spending are most urgently needed.

The Stories We Are Told

The relationships between employment, productivity, supply chains, money supply, inflation, interest rates, and the risks of manipulation or speculation have long preoccupied economists and bankers yet remain difficult to pin down. Taken together, these episodes show that modern economies have become both organized around, and constrained by, interest as their central coordinating mechanism. The decade of cheap money did not deliver a fairer or more productive system. Within this mix, the interest rate itself raises basic questions: is it a real signal emerging from market forces, or an artificial lever that appears easy to adjust but proves weak at shaping everything else? What purpose does it serve, how does it shape the everyday lives of both rich and poor, and what would happen if we tried to make interest obsolete as a guiding tool for the modern economy? Join us to explore this further.

References

Federal Reserve Board historical federal funds target rate data from 2008 onward

European Central Bank deposit facility rate history

Bank of Japan policy rate history and March 2024 exit from negative rates

S&P Dow Jones Indices information on the S&P 500

S&P 500 historical levels via Federal Reserve Economic Data

S&P CoreLogic Case-Shiller US National Home Price Index

Freddie Mac Primary Mortgage Market Survey

Bank for International Settlements research on credit cycles and financial stability

World Bank International Debt Statistics and external debt data

IMF analysis on spillovers from US news and monetary policy to emerging markets

Habeeb Yahya is a volunteer post-doctoral research fellow at MyLLife. He is formally affiliated with University of Turku, Finland conducting empirical research and teaching courses at both bachelor’s and master’s level at the Turku School of Economics.

Rashed Hasan is the Director of Research at MyLLife and its Founder Director. He is a Professor of Practice at George Mason University’s School of Business, a former tech entrepreneur, management consultant, Sr. Business Executive, and an Author.