How a simple change to accounting rules could end the era of mass layoffs as a financial strategy — and why it has not happened yet.

First, a Quick Lesson in How Company Books Actually Work

You don't need an MBA for this.

When a company spends money, accountants ask one question: expense or investment? An expense is consumed now and reduces this year's profit. An investment produces value over time and sits on the balance sheet as an asset, depreciated gradually through the income statement.

Under current rules, every dollar spent on employees is an expense. Salaries, training, onboarding, years of accumulated institutional knowledge built by a senior engineer — all of it disappears into the cost column, reducing profits immediately, never appearing on the balance sheet.

When you cut a cost, profits go up. Immediately. Visibly. In ways investors can see and reward.

This isn't a bug in the system. It's a feature — one designed in a different era for a different kind of economy.

The World Has Changed. The Rulebook Hasn't.

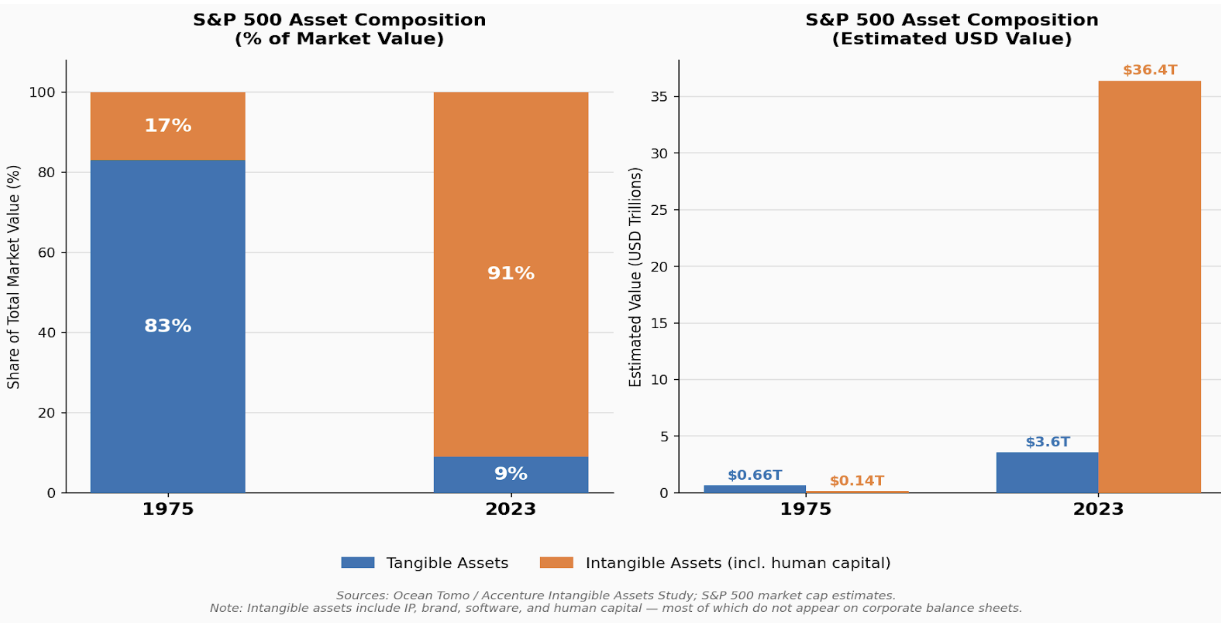

In 1975, physical assets (factories, machinery, raw materials) made up about 83% of the value of S&P 500 companies. By 2023, that ratio had mostly flipped: intangible assets — brand, intellectual property, software, and human talent — accounted for roughly 91% of major corporate value.

Meta doesn't manufacture anything you can hold. Its "factories" are the engineers who build the algorithms, the product managers who shape the roadmap, the researchers who push the frontier. Under GAAP, none of that human capability appears anywhere on the balance sheet.

When companies capitalize software they build, or patents they develop, destroying them triggers an impairment charge: an official recognition that something of value was lost. When companies lay off workers? Nothing. No asset to impair. Just a smaller expense line and a better-looking margin.

Humans Aren't the Only Missing Asset

It's worth noting that human capital isn't uniquely singled out. Under GAAP, most internally generated intangibles are expensed rather than capitalized — a brand built over decades, customer relationships cultivated organically, internally developed trade secrets. The broader rule is this: if you acquired it through a purchase or merger, you can capitalize it. If you built it yourself, you generally cannot.

This creates a specific distortion. A company that acquires a workforce through an acquisition must capitalize the associated value as goodwill. A company that builds the same workforce organically reports it as nothing. Human capital accounting is one piece of a broader problem: the rulebook doesn't reflect how modern companies actually create value.

Enter the Human Capital Model

A framework developed by economists Baruch Lev and Aba Schwartz proposed treating the workforce as an intangible asset, valued by estimating the future economic contribution of employees over their expected tenure, not unlike how we value any long-term investment.

Applied to Meta, using conservative assumptions:

~67,000 employees

Average total compensation (salary, bonus, stock): $220,000/year

Average expected tenure: 4 years

Discount rate: 8.5%

That yields approximately $720,000 in human capital value per employee — a conservative estimate of present-value contribution over their tenure. Multiply across 67,000 people and you get roughly $48 billion in human capital assets.

For comparison: Meta's total reported assets are around $250 billion, to which the workforce currently contributes exactly zero. Under a human capital model, people would represent about 16% of the company's entire asset base. That's not a rounding error. That's a fundamentally different picture of what the company is.

Current Rules (GAAP) | Human Capital Model | |

Buildings, servers, cash & investments | $250 billion | $250 billion |

Workforce | $0 | $48 billion |

Total Assets | $250 billion | $298 billion |

And the Income Statement, Too

The distortion runs beyond the balance sheet. Under current rules, every investment in people hits the income statement immediately. Training a new engineer costs $50,000 — that reduces this year's earnings, even though the productivity benefit plays out over years. Recruitment, onboarding, skills development: all treated identically to buying printer paper.

Under a human capital framework, investment-like expenditures would be capitalized and amortized — exactly how companies already treat software development costs under ASC 350. Routine compensation stays as an expense. What changes is the treatment of outlays that create lasting value.

When layoffs occur, the income statement would carry an impairment charge: not merely a reduction in payroll expense, but a formal recognition that productive capacity has been destroyed.

Financial Statement | Current Rules (GAAP) | Human Capital Model |

Balance sheet | Workforce: $0 | Workforce: ~$48B asset |

Income statement | All employee costs expensed immediately; no impairment on layoffs | Investment costs amortized over tenure; impairment charge on material layoffs |

Cash flow statement | All workforce spend: operating outflow | Development spend reclassified to investing; impairments appear as non-cash charge |

The Layoff Math, Rewritten

Meta eliminated approximately 21,000 jobs in its "Year of Efficiency." Under current rules: reduced expenses, higher margins, investor applause.

Under a human capital model, those 21,000 employees represented real capital. At $720,000 per person:

21,000 employees x $720,000 = approximately $15 billion in asset impairment.

Current Rules | Human Capital Model | |

What a layoff looks like | Expense reduction | Asset impairment |

Effect on earnings | Margins improve | Impairment charge recognized |

Signal to investors | “We got efficient” | “We reduced capacity” |

Capability loss | Invisible | Reported on the books |

If Meta had demolished $15 billion worth of data centers to cut costs, the financial statements would record a devastating loss and everyone would ask hard questions. When 21,000 people walked out the door, the books recorded it as a win.

How This Changes What Executives Think About

Under the current system, the fastest path to a higher stock price is often a workforce reduction: fast, visible, and immediately rewarded by the accounting. Training programs reduce profits this quarter. Retention bonuses are added expense. Culture that keeps talent around doesn't show up in the numbers.

Under a human capital framework, those incentives shift. Training becomes an investment that builds asset value. Losing a senior engineer isn't just a talent problem — it's a capital loss. A restructuring that triggers $15 billion in impairment charges is a very different conversation at the board level than one framed as "improving efficiency."

The question executives ask changes from "How do we reduce expense?" to "How do we get a better return on our human capital?" Same competitive pressure. Very different path.

What About Workers?

This framework does not guarantee job security. Companies will still face competition. Investors will still demand returns. Sometimes restructuring is genuinely necessary.

What it changes is the narrative around workforce decisions. Right now, layoff announcements use language like "streamlining operations" — treating people as overhead to be optimized. Under a human capital model, the same announcement would require acknowledging that the company is destroying assets and recognizing a financial cost in the earnings, not just a human cost in the headlines.

When the numbers say "we got more efficient," the story is over. When the numbers say "we recognized a $15 billion capital loss," the story has just begun.

What Would Actually Change: The View from Each Seat

The CEO

Under a human capital model, cutting 10,000 jobs triggers a visible impairment charge requiring explanation to the board and investors — not just a margin improvement on an earnings call. Training spend shifts from "expense to minimize" to "investment in an appreciating asset." The incentive structure changes before the decision is made.

The Financial Analyst

Analysts already back out non-cash charges when modeling companies. There is a real risk human capital impairments get added to the "noise" stripped from adjusted earnings. But formalizing human capital metrics on the balance sheet also gives analysts a standardized basis for comparison, a way to flag companies harvesting their workforce for short-term gains, and a more complete picture of what a restructuring actually costs.

Society

Mass layoffs are social events as much as financial ones. A human capital model doesn't capture the full social cost of 20,000 families disrupted, but it begins to internalize what the current framework treats as pure externality. When the accounting system acknowledges that something real was lost, it changes what boards, investors, and executives feel accountable for.

The Policymaker

The SEC's 2020 human capital disclosure requirements were a step forward, but they produce inconsistent, unauditable narratives rather than comparable numbers. Standardized capitalization rules would give regulators audited data on how companies invest in or disinvest from their workforces. Tax implications follow — but those are design questions, not reasons to avoid the reform.

The Criticisms Worth Taking Seriously

Measurement is genuinely hard

Unlike a building with a purchase price, human capital value is estimated, not observed. Different assumptions about tenure, productivity, and discount rates yield very different numbers. The same workforce could be valued at $30 billion or $80 billion depending on inputs, creating complexity for preparers and ample opportunity for manipulation.

People aren't property

There is something genuinely uncomfortable about listing a workforce as a $48 billion asset. Employees can quit on a Monday morning. They can't be possessed like a factory. Critics argue this framing reduces a human relationship to an inventory item.

Non-cash charges are easy to ignore

If impairment charges are non-cash, investors may simply strip them from adjusted earnings — as they routinely do with goodwill write-downs. There's no guarantee human capital impairments would be treated differently.

Volatility and gaming

Human capital assets would fluctuate with hiring cycles, attrition, and compensation changes. Wherever there is an accounting choice, there is an incentive to optimize for appearance: inflating tenure assumptions, understating discount rates, or timing layoffs to minimize reported impairments.

Despite these criticisms, the question is no longer whether human capital matters to firm value. It clearly does. The criticisms define the design problem. They don't make the status quo defensible.

The Deeper Problem with "Efficiency"

Meta's mass layoffs were called efficient, and the stock market confirmed it. But efficiency means getting more output from the same input — not simply cutting input and hoping output holds up. When a company eliminates thousands of experienced engineers, it also loses institutional knowledge that took years to build, mentors who developed junior talent, and teams whose output depends on trust and shared context. It signals to remaining employees that they too are ultimately expendable.

None of those costs appear in GAAP earnings. They're pushed into the future, or onto the workers themselves. Human capital accounting doesn't capture everything — no system does. But it forces some of that invisible cost into the visible record, which forces it into the conversation.

Conclusion: The Books Are Telling the Wrong Story

Meta's "Year of Efficiency" was celebrated because the numbers said it was efficient. The numbers were telling an incomplete story.

Under a human capital framework, the same period reads differently: margins improved, but $15 billion in productive capacity was dismantled. The workers who left took with them expertise, relationships, and institutional knowledge that had real economic value — value that simply vanished from the official record.

Accounting doesn't just describe companies. It shapes them. It tells executives what to optimize for, tells investors what to reward, tells boards what questions to ask.

In an economy where human talent is the primary driver of value, financial statements that treat those humans as overhead are not neutral tools. They are a thumb on the scale.

Recognizing employees as assets wouldn't end layoffs. The criticisms are real, the measurement challenges genuine, and any reform would require careful design. But right now, the books don't even try to count the cost honestly.

And right now, we are not.

Methodology note

This article applies a simplified Lev-Schwartz human capital valuation framework to Meta's publicly reported workforce and compensation data. Asset composition percentages are based on Ocean Tomo / Accenture Intangible Assets Study data; dollar figures represent illustrative estimates derived from approximate S&P 500 market capitalization for the reference years. All figures are for analytical purposes only.

Dominic Leone: Graduate Research Intern at MyLLife Inc., and MBA from GMU School of Business. Rashed Hasan: Founder & Director, MyLLife Inc., Alexandria, VA, and Professor of Practice, Management and Finance, George Mason University, Fairfax, VA