Zakat is one of the Five Pillars of Islam, obligating Muslims who possess wealth above the nisab to donate 2.5% of that wealth annually to eligible recipients 1. The Islamic Development Bank estimates the global annual potential at between $200 billion and $1 trillion, depending on methodology, though reliable national-level figures are scarce 2.

Yet the gap between potential and realised collection is vast. In nearly every country where Zakat data exists, formal institutions — whether state-run, semi-public, or civil-society-led — capture only a small proportion of what payers actually give. The remainder flows informally: directly to family members, community religious figures, local mosques, or individuals the donor personally trusts. This phenomenon is not unique to any single political system or income level; it appears in high-income Gulf states as readily as in middle-income Southeast Asian nations 3.

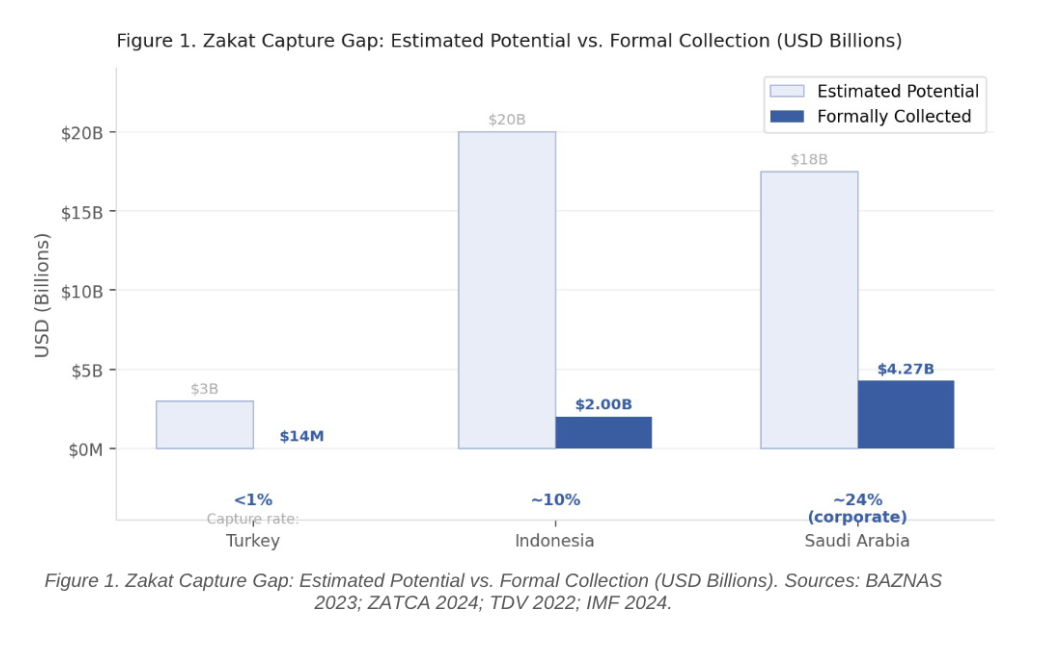

This article examines three countries that together span the full spectrum of governance approaches: Turkey (NGO-led voluntarism), Indonesia (hybrid state-civil coordination), and Saudi Arabia (mandatory state enforcement). Combined, they account for approximately 358 million Muslims and a combined GDP of $3.55 trillion. Their Zakat systems could, in principle, mobilise an estimated $37–44 billion annually, yet formal collection across all three amounts to roughly $6.3 billion, or less than 17% of the lower-bound estimate 4,5,6.

Global Zakat Context and the Three-Country Rationale

Zakat differs fundamentally from voluntary charity (sadaqah) in that it is a religious obligation, not a choice. Unlike income taxation, it applies to accumulated wealth — cash, gold, silver, livestock, trade goods, and investment assets — that has been held above the nisab for a full lunar year 1. This means the Zakat base is potentially far larger than income-based transfer systems, as it targets stock rather than flow.

Academic estimates of global Zakat potential vary widely because qualifying wealth is difficult to measure. A widely-cited Islamic Research and Training Institute (IRTI) study estimated the global potential at $200–250 billion per year 2, while more optimistic estimates that include agricultural and business asset Zakat reach above $500 billion 7. What is consistent across estimates is the capture gap: formal collection globally is believed to fall below 10% of the potential 3.

Why These Three Countries

Turkey, Indonesia, and Saudi Arabia were selected because they collectively represent the three dominant institutional models, span three continents, and possess relatively reliable administrative data. They also show the independence of institutional design from per-capita wealth: Saudi Arabia's GDP per Muslim ($33,300) is nearly six times Indonesia's ($5,700), yet both have large uncaptured Zakat pools 4,5,6. Turkey, despite a per-capita figure of $12,700 4, has the lowest formal capture rate of the three, primarily because it has the least institutional infrastructure.

Metric | Turkey | Indonesia | Saudi Arabia |

GDP (2024 USD) | $1.08T | $1.37T | $1.10T |

Muslim population | ~85M (99%) | ~240M (87%) | ~33M (97%) |

GDP per person (USD) | ~$19,018 | ~$5,362 | ~$37,811 |

GDP per Muslim (USD) | ~$12,700 | ~$5,700 | ~$33,300 |

Governance model | NGO-led (TDV) | Hybrid: BAZNAS + LAZ | State authority (ZATCA) |

Legal enforcement | None | Partial (Law 23/2011) | |

Formal collection (USD) | ~$14.2M | ~$2.0B | ~$4.27B |

Estimated potential (USD) | ~$2–4B | ~$20B | ~$15–20B |

Capture rate | <1% | ~10% | High (corporate only) |

Turkey: Community Trust Without Institutional Scale

Turkey’s Zakat system is the most decentralized among the countries studied, with no legal obligation, regulatory framework, or central authority overseeing its collection or distribution. Instead, Zakat is treated as a private religious practice, typically carried out through informal, trust-based networks such as local mosques, neighborhood associations, and personal connections 8.

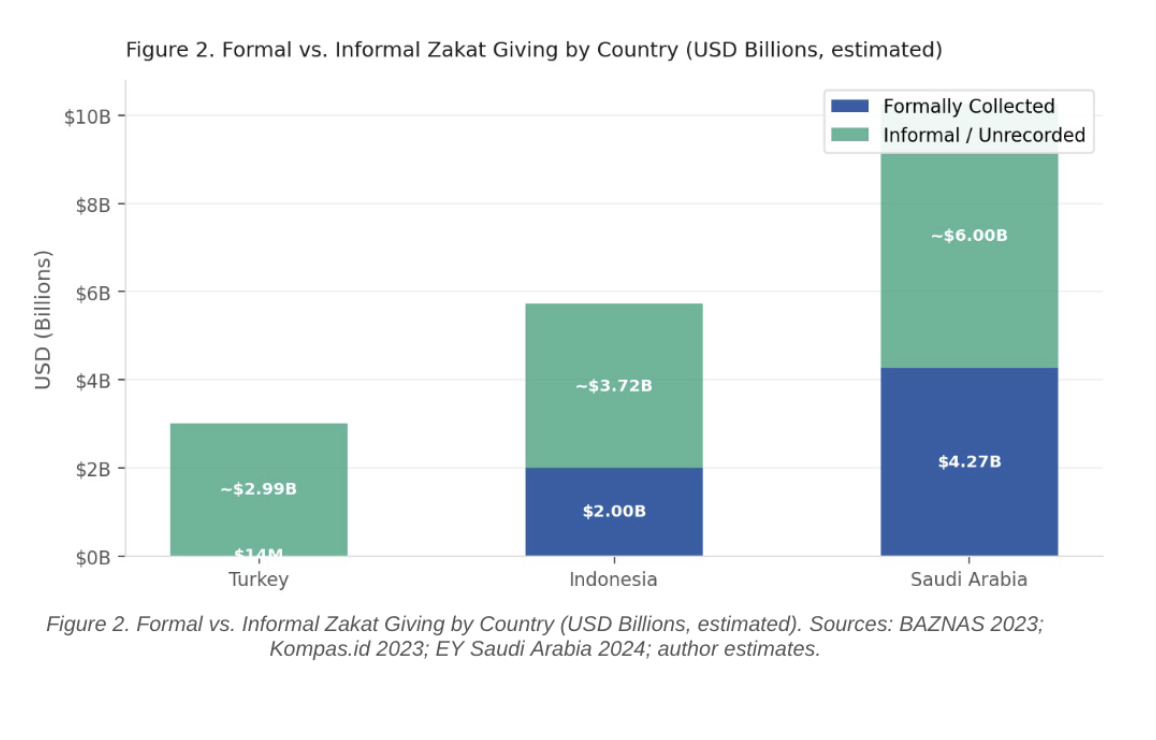

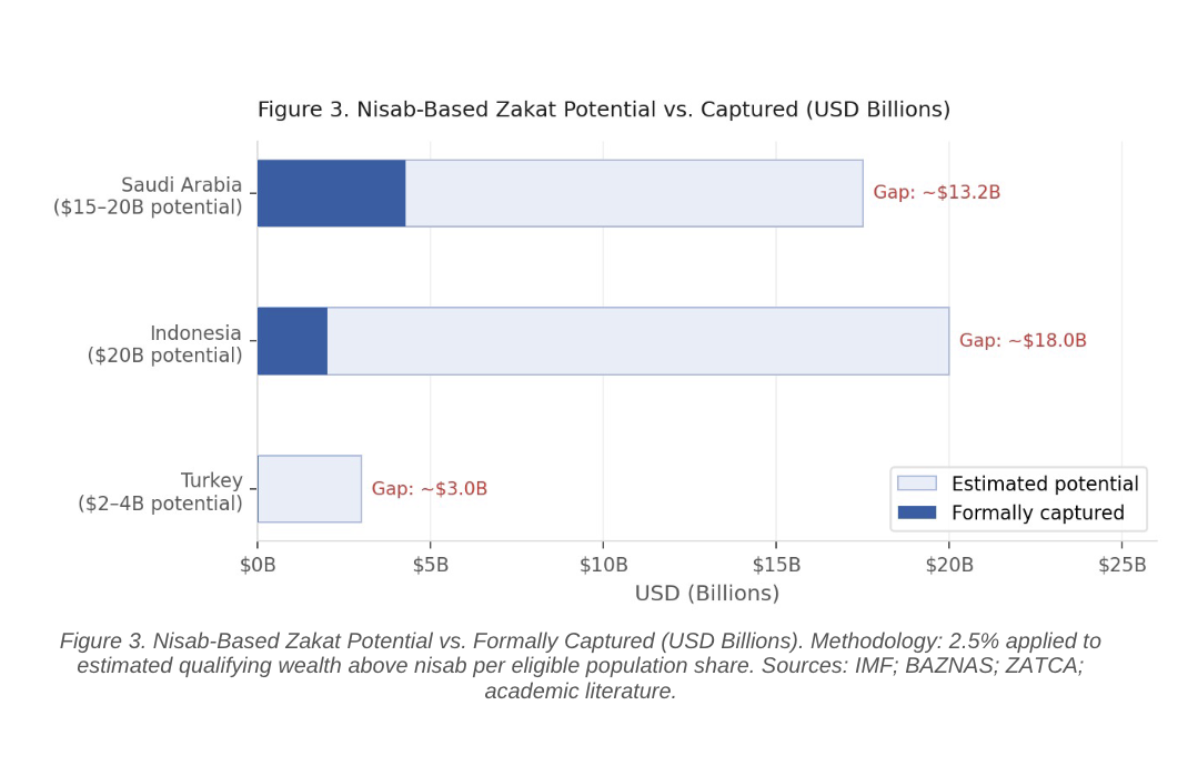

The main formal institution involved is the Türkiye Diyanet Foundation (TDV), which is affiliated with—but legally independent from—the state’s Directorate of Religious Affairs. TDV facilitates Zakat contributions through branches, digital platforms, and outreach efforts, yet it lacks any enforcement authority. In 2022, it collected around $14.2 million, a figure that has remained relatively stable over time 9. Despite this modest collection, TDV demonstrates strong operational efficiency, delivering humanitarian aid across 149 countries and reaching over two million beneficiaries each year, largely due to low administrative costs and reliance on volunteer networks. However, this formal collection represents only a tiny fraction of Turkey’s estimated Zakat potential of $2–4 billion annually, indicating a capture rate of less than 1%, with the vast majority of giving remaining informal and outside institutional channels 4,10.

Turkey's voluntary model generates notably high community trust. Donors who give through TDV or local networks report confidence that their Zakat reaches legitimate recipients, a sentiment that is harder to sustain in larger bureaucratic systems 10. The system's central weakness is its inability to aggregate giving at scale. Because there is no central registry and no coordination between the dozens of NGOs collecting Zakat-like donations, data on total giving is unavailable. This makes impact measurement impossible and prevents the kind of beneficiary targeting that could maximise poverty-reduction outcomes 8.

Metric | Value |

Muslim population | ~85 million (99% of total) |

GDP per Muslim (USD) | ~$12,700 |

Formal Zakat collected — TDV (2022) | ~$14.2 million USD |

Estimated annual Zakat potential | ~$2–4 billion USD |

Capture rate (formal/potential) | <1% |

Countries served by TDV | 149 |

Beneficiaries reached annually | 2 million+ |

Central Zakat registry | None |

Legal enforcement mechanism | None |

Indonesia: Institutional Scale Without Full Trust

Indonesia has the most institutionally developed Zakat system among the three countries, built around a formal legal framework established by Law No. 23 of 2011. This framework created a dual structure in which BAZNAS, the national state body, oversees Zakat collection, distribution, and reporting, while licensed private institutions (LAZ) operate alongside it under BAZNAS supervision 11. The law marked a major step toward formalization by mandating payroll-based Zakat contributions for government employees, introducing national reporting standards, and regulating private Zakat organizations through licensing. As a result, formal participation has expanded significantly, with 28.1 million registered Zakat payers by 2024 5. However, trust remains a key constraint, as many Indonesians continue to prefer giving through local religious leaders, pesantren networks, and community channels rather than formal institutions.

Operationally, Indonesia’s formal Zakat sector has experienced rapid growth, with total collections reaching about IDR 33 trillion (approximately $2 billion USD) in 2023, a substantial increase from a decade earlier. This expansion has been driven largely by digital payment integration, with platforms such as GoPay, OVO, Dana, and major banks making contributions easier, particularly for younger and urban populations 12. Despite these gains, formal Zakat collection still represents only around 10% of the country’s estimated potential of IDR 327 trillion (about $20 billion USD). A large informal sector persists, estimated at IDR 61 trillion (roughly $3.7 billion USD), flowing through community-based networks that often enjoy stronger donor trust due to their personal and localized nature 13.

Metric | Value |

Muslim population | ~240 million (87% of total) |

GDP per Muslim (USD) | ~$5,700 |

Estimated Zakat potential | ~IDR 327 trillion (~$20.0B USD) |

Formal collection — BAZNAS + LAZ (2023) | ~IDR 33 trillion (~$2.0B USD) |

Capture rate (formal/potential) | ~10% |

Informal giving estimate | ~IDR 61 trillion (~$3.7B USD) |

Registered Zakat payers (2024) | 28.1 million |

Governing legislation | Law No. 23 of 2011 |

Primary digital channels | GoPay, OVO, Dana, bank transfer |

Saudi Arabia: Administrative Precision, Incomplete Coverage

Saudi Arabia operates the most centralized and legally enforced Zakat system, where payment is a constitutional obligation administered by the Zakat, Tax, and Customs Authority (ZATCA). The system functions similarly to corporate taxation: Saudi-owned companies and GCC shareholders must file annual declarations, pay assessed amounts through a fully digital platform, and are subject to audit and penalties for non-compliance 14. This high level of formalization and digitization has driven strong corporate compliance and resulted in the largest formal Zakat collection among the countries studied—around SAR 16 billion ($4.27 billion) in 2024 15. Zakat distribution is integrated into the national welfare system, improving administrative efficiency and alignment with state social programs, though public transparency on outcomes remains limited 6.

Despite this strong institutional framework, a major gap exists in the near-total exclusion of individuals. Personal Zakat is treated as a private religious obligation, with no formal reporting, verification, or enforcement, and non-Saudi residents are largely outside the system altogether. As a result, while corporate contributions are effectively captured, a significant share of potential Zakat—particularly from wealthy individuals holding assets in cash, gold, and investments—remains untapped 14.

Metric | Value |

Muslim population | ~33 million (97% of total) |

GDP per Muslim (USD) | ~$33,300 |

Formal Zakat collection (2024) | SAR 16B (~$4.27B USD) |

Estimated total Zakat potential | ~$15–20 billion USD |

Collection scope | Corporate mandatory; individual informal |

Collection method | Digital self-assessment via ZATCA portal |

Distribution mechanism | Integrated into national welfare system |

Individual Zakat formal status | Outside formal system (self-compliance assumed) |

Non-Saudi resident inclusion | Largely excluded (~38% of population) |

The Zakat Capture Gap

D

D

How the Potential Estimates Are Calculated

Zakat potential estimates rely on the following standard methodology: (1) identify the Muslim population, (2) estimate the share of that population whose net wealth exceeds the nisab threshold (~$5,000 USD equivalent), (3) apply the 2.5% Zakat rate to the estimated average qualifying wealth of eligible individuals, and (4) aggregate across the population 2,7. The table below summarises the inputs used in this study.

Input Variable | Turkey | Indonesia | Saudi Arabia |

Muslim population | ~85M | ~240M | ~33M |

Est. % above nisab threshold | ~25–35% | ~15–20% | ~60–70% |

Average qualifying wealth (USD) | ~$18,000 | ~$7,000 | ~$70,000 |

Zakat rate | 2.5% | 2.5% | 2.5% |

Annual potential (USD) | ~$2–4B | ~$20B | ~$15–20B |

Formally captured (USD) | ~$14.2M | ~$2.0B | ~$4.27B (corporate) |

Uncaptured gap (USD) | ~$2–4B | ~$18B | ~$11–16B |

Cross-Country Comparison

Dimension | Turkey | Indonesia | Saudi Arabia |

Governance model | NGO-led (TDV) | Hybrid: BAZNAS + LAZ | State authority (ZATCA) |

Legal enforcement | None | Partial (Law 23/2011) | Constitutional mandate |

Collection scope | Voluntary individuals only | Individual + corporate (partial) | Corporate mandatory; individual informal |

Digital infrastructure | Low — no central platform | Growing — mobile wallets integrated | High — fully digitised self-assessment |

Transparency & reporting | Low; fragmented NGO reporting | Moderate; BAZNAS publishes annual reports | Limited; distribution reporting opaque |

Beneficiary registry | None | Partial (BAZNAS-registered) | National welfare registry (ZATCA) |

Formal collection (USD) | ~$14.2M | ~$2.0B | ~$4.27B |

Estimated potential (USD) | ~$2–4B | ~$20B | ~$15–20B |

Capture rate | <1% | ~10% | High (corporate); low (individual) |

Informal giving (USD est.) | ~$2–4B (dominant) | ~$3.7B (very large) | Substantial (individual wealth) |

Community trust level | High (local networks) | Mixed; trust deficit in BAZNAS | Institutional; limited community feel |

Global humanitarian reach | Highest (149 countries) | Primarily domestic | Significant, government-coordinated |

The Core Problem: Trust, Not Generosity

A recurring theme across all three country cases is that the principal constraint on formal Zakat collection is not donor compliance with the religious obligation, but donor confidence in the institution receiving the funds. Across Turkey, Indonesia, and Saudi Arabia, survey and observational data consistently show that Muslims give Zakat at substantial rates — but that a large proportion of this giving bypasses formal channels 3,10,13.

The three country cases illustrate this dynamic distinctly. In Turkey, trust exists at the local level — in the imam, the mosque committee, the neighbourhood association — but does not transfer to national institutions, which remain too remote and too unaccountable to command it 8. In Indonesia, BAZNAS has built legal infrastructure but has not yet resolved a persistent public perception that bureaucratic Zakat distribution is subject to leakage and misallocation 13. In Saudi Arabia, individual donors operate under an assumption of self-compliance that is essentially unverifiable, and without community-level institutions to anchor trust, personal Zakat has become entirely privatised 14,15.

Best Practices and Lessons Learned

What Each System Does Well

Country | Institutional Best Practice | Replicable Lesson |

Turkey (TDV) | Community-first trust architecture: 2M+ beneficiaries across 149 countries on $14.2M formally collected — exceptional distribution leverage | Voluntary systems embedded in trusted community networks can achieve outsized humanitarian impact; local trust is the foundation, not the ceiling |

Indonesia (BAZNAS) | Legal and digital scaffolding: fastest-growing formal Zakat sector in the Muslim world, driven by payroll deduction, mobile wallet integration, and a national legal framework | Statutory legitimacy combined with frictionless digital payment creates scalable collection growth; payroll deduction alone raised government-employee compliance dramatically |

Saudi Arabia (ZATCA) | Administrative precision: full digitisation of corporate Zakat filing, audit-backed enforcement, and integration with national welfare distribution — highest absolute formal collection globally | Mandatory digital self-assessment with audit capability and penalty enforcement achieves consistent corporate compliance without requiring voluntary trust; welfare integration eliminates distribution duplication |

A Policy Framework for Closing the Gap

Drawing on the comparative evidence, we identify seven priority reforms that would materially improve formal Zakat capture without sacrificing the community trust that sustains voluntary giving.

Reform Priority | Problem Addressed | Modelled On |

Mandatory independent audits and public annual reports | Rebuilds institutional trust; reduces informal bypass among sceptical donors | Indonesia (BAZNAS reporting) — strengthened with external audit requirement |

National beneficiary registries linked to welfare systems | Eliminates leakage; enables needs-based targeting; demonstrates distribution efficacy to donors | Saudi Arabia's ZATCA-welfare integration, extended to individual Zakat |

Interoperable digital payment ecosystems | Reduces transaction friction; extends reach to diaspora, younger donors, and rural populations | Indonesia's GoPay/OVO/bank integration — scaled nationally |

Protection and formalisation of local trust networks | Maintains community participation; prevents alienation from top-down mandates; preserves giving culture | Turkey's mosque-community model, with standardised reporting requirements |

Individual Zakat voluntary declaration frameworks | Opens formal channel for personal wealth Zakat without coercive enforcement | Hybrid: Saudi administrative infrastructure + Indonesian statutory basis |

Cross-border coordination mechanisms for diaspora Zakat | Channels diaspora giving to origin-country programmes; reduces informal transfer losses | TDV's global humanitarian model, systematised with government coordination |

Standardised national Zakat accounting standards | Enables reliable impact measurement; supports cross-country benchmarking and donor confidence | New development — no country has implemented this comprehensively |

Conclusion: Unlocking a $37–44 Billion Institution

Across all three cases, the combined annual Zakat potential is estimated at $37–44 billion USD 4,5,6,7. Current formal collection totals approximately $6.3 billion — roughly 15–17% of the lower bound. The uncaptured $30+ billion represents a profound welfare transfer that could, if mobilised, dwarf the foreign aid flows received by many Muslim-majority countries.

The path to mobilising that potential does not run through heavier enforcement or tighter state control. It runs through institutional credibility: transparent reporting, auditable distribution, community-embedded delivery, and systems so demonstrably effective that informal giving migrates to them voluntarily. The governance tools exist. What remains is the political will and institutional commitment to apply them 16,17.

References

1. Kahf, M. (1999). Zakat: Unresolved Issues in the Contemporary Fiqh. Journal of Islamic Economics, 2(1), 1–22.

2. Islamic Research and Training Institute / Islamic Development Bank (IRTI). (2015). Zakat in the 21st Century: Potential and Development. Jeddah: IDB.

3. Shirazi, N. S., & Amin, M. F. (2009). Poverty Elimination through Potential Zakat Collection in OIC Countries: Revisited. Pakistan Development Review, 48(4), 739–754.

4. International Monetary Fund. (2024). World Economic Outlook: GDP per capita and Wealth Distribution Data. Washington, DC: IMF.

5. Badan Amil Zakat Nasional (BAZNAS). (2023). Statistik Zakat Nasional 2023 [National Zakat Statistics 2023]. Jakarta: BAZNAS.

6. Zakat, Tax and Customs Authority (ZATCA). (2024). Annual Zakat Collection Report 2024. Riyadh: ZATCA.

7. Obaidullah, M., & Khan, T. (2008). Islamic Microfinance Development: Challenges and Initiatives. Islamic Research and Training Institute Policy Dialogue Paper No. 2.

8. Türkiye Diyanet Foundation (TDV). (2022). TDV Annual Report 2022: Zakat and Humanitarian Operations. Ankara: TDV.

9. Daily Sabah. (2023). Turkey's charitable landscape: TDV and the NGO Zakat ecosystem. Istanbul: Daily Sabah.

10. Çizakça, M. (2000). A History of Philanthropic Foundations: The Islamic World from the Seventh Century to the Present. Istanbul: Boğaziçi University Press.

11. Republic of Indonesia. (2011). Law No. 23 of 2011 on Zakat Management (Undang-Undang No. 23 Tahun 2011 tentang Pengelolaan Zakat). Jakarta: State Gazette.

12. Kompas.id. (2023). Digitalisasi Zakat: Pertumbuhan dan Tantangan [Zakat Digitalisation: Growth and Challenges]. Jakarta: Kompas.

13. Firdaus, M., Beik, I. S., Irawan, T., & Juanda, B. (2012). Economic Estimation and Determinations of Zakat Potential in Indonesia. Islamic Research and Training Institute Working Paper No. 1433-7.

14. Saudi Arabia Basic Law of Governance (Royal Decree No. A/90, 1992), Article 20. Riyadh: Kingdom of Saudi Arabia.

15. EY Saudi Arabia. (2024). Zakat Regulatory Update: ZATCA Developments and Corporate Compliance Guidance. Riyadh: Ernst & Young.

16. Torgler, B. (2006). The importance of faith: Tax morale and religiosity. Journal of Economic Behavior & Organization, 61(1), 81–109.

17. Kirchler, E. (2007). The Economic Psychology of Tax Behaviour. Cambridge: Cambridge University Press.

If you found this article informative & would like to support further research, click here to donate!